Businesses need finance, or money, to pay for their overhead costs as well as their day to day and variable expenses. Here are three situations when businesses need finance the most:

- Starting a business: Huge amounts of finance is needed to start a business which requires buying fixed assets, paying rent and other overheads as well as producing or buying the first products to sell. The finance required to start up a business is called start-up capital.

- Expanding a business: When expanding, a lot of capital is needed in order to buy more fixed assets or fund a takeover. Internal growth by developing new products also requires a notable amount of finance for R&D.

- A business in difficulties: For example, for loss making businesses money is needed to buy more efficient machinery, or money is needed to cover negative cash flow. However, it is usually difficult for these firms to get loans.

All all cases, businesses need finance for either capital expenditure or revenue expenditure:

- Capital expenditure: Money spent on fixed assets.

- Revenue expenditure: Money spent on day-to-day expenses.

Sources of finance

There are many ways to obtain finance, and they can be grouped in these ways.:

- Internal or external.

- Short-term, medium-term or long-term.

Internal finance:

This is finance that can be taken from within the business itself. There are advantages and disadvantages to each of them:

- Retained profit: Profit reinvested into a business after part of the net profit has been distributed to its owners.

- + Retained profit does not have to be repaid unlike a loan.

- - New businesses do not have much retained profit.

- - Retained profit from small firms are not enough for expansion.

- - Reduces payment to owners/shareholders.

- Sale of existing assets: Firms can get rid of their unwanted assets for cash.

- + Makes better use of capital that is not used for anything.

- - Takes time to sell all of these assets.

- - New businesses do not have these assets to sell.

- Running down stocks: Sell everything in the current existing inventory.

- + Reduces opportunity cost and storage costs of having inventory.

- - Risks disappointing customers if there are not enough stock left.

- Owners' savings: Only applies to businesses that do not have limited liability. Since the legal identity of the business and owners are the same, this method is considered to be internal.

- + Available quickly.

- + No interest paid.

- - Limited capital.

- - Increases risks for owners.

External finance:

This is money raised from individuals or organisations outside a business. It is the most common way to raise finance.

- Issue of shares: Same as owners' savings, but only available to limited companies.

- + A permanent source of capital that does not have to be repaid.

- + No interest paid.

- - Dividends will have to be paid.

- - Ownership of the company could change hands to the majority shareholder.

- Bank loans: money borrowed from the bank.

- + Quick to arrange.

- + Variable lengths of time.

- + Lower rates offered if a large company borrows large sums.

- - Must be repaid with interest.

- - Collateral is needed to secure a loan and may be lost.

- Selling debentures: These are long-term loan certificates issued by limited companies.

- + These can be used to raise long-term finance, e.g. 25 years.

- + No collateral is required, just the trustworthiness of a big company.

- - Must be repaid with interest.

- Factoring of debts: Some businesses (debt factors) "buy" debts of a firm's debtors (e.g. customers) and pay the firm cash in return. The firm now does not worry about worrying about whether their customers will pay or not and 100% of all the debts goes to the factor. Factoring debt is very difficult for me to understand and explain, so explore http://business-debt.cleardebts.co.uk/factoring.html for more information.

- + Immediate cash is obtained.

- + Risk of collecting debt becomes the factor's.

- - The firm does not receive 100% value of the debt.

- Grants and subsidies: can be obtained from outside agencies like the government.

- + Do not have to be repaid.

- - They have conditions that you have to fulfill (e.g. locating in poor areas).

Short-term finance:

This is working capital required to pay current liabilities that is needed up to three years. There are three main ways of acquiring short-term finance:

- Overdrafts: Allows you do draw more from your bank account than you have.

- + Overdrafts can vary every month, making it flexible.

- + Interest only needs to be paid only to the amount overdrawn.

- + They can turn out cheaper than loans.

- - Interest rates are variable, and often higher than loans.

- - The bank can ask for the overdraft back immediately anytime.

- Trade credits: Delaying payment to your creditors, which leaves the company with better cash flow for that month.

- + It is almost a short-term interest free loan.

- - The supplier could refuse to give discounts or to supply you at all if your payments are delayed too much.

- Factoring of debts

Finance available for 3 to 10 years that is used to buy fixed assets such as machinery and vehicles.

- Bank loans

- Hire purchase: This allows firm to pay for assets over time in monthly payments which has interest.

- + The firm does not have to come up with a lot of cash quickly.

- - A deposit has to be paid at the start of the period of payment.

- - Interest paid can be very high.

- Leasing: Hiring something. Businesses could use the asset but will have to pay monthly. The business my choose to buy the asset at the end of the leasing period. Some businesses sell their fixed assets to a leasing company who lease them back so that they could obtain cash. This is called sale and leaseback.

- + The firm does not have to come up with a lot of cash quickly.

- + The leasing firm takes care of the assets.

- - The total leasing costs will be higher than if the business has purchased it.

Long-term finance:

This kind of finance is available for more than 10 years. The money is used for long-term fixed assets or the takeover of another company.

- Issue of shares: Shares are sometimes called equities, therefore issuing shares is called equity finance. New issues, or shares sold by public limited companies can raise near limitless finance. However, a business will want to give the right issue of shares so that the amount bought by shareholders will not upset the balance of ownership.

- + A permanent source of capital that does not have to be repaid.

- + No interests paid.

- - Dividends will have to be paid. And they have to be paid after tax (so taxes become higher), while interest on loans are paid before taxes.

- - Ownership of the company could change hands to the majority shareholder.

- Long-term loans or debt finance: Loans from a bank, and this is how they are different from issuing shares:

- Interest is paid before taxes, it is counted as an expense.

- Interest has to be paid every year but dividends only need to be paid if the firm has maid profit.

- They are not permanent capital.

- They need collateral.

- Debentures

How the choice of finance is made in a business

These are the factors that managers consider when choosing the type of finance they need.

- Purpose and time period: Managers need to match the source of finance to its purpose. It is quite simple, short-term finance is used to buy current assets and things like that, while long-term finance for fixed assets and similar things.

- Amount needed: Different types of finance depends on how much is needed.

- Status and size: Bigger companies have more choices of finance. They pay less interest to banks.

- Control: owners lose control if they own less than 51% of shares in their company.

- Risk and gearing: loans raise the gearing of a business, meaning that their risk is increased. Gearing is can be obtained by calculating the percentage of long-term loans compared to total capital. If long-term loans take up more than 50% of total capital, then the business would be called highly geared. This is very risky because the business will have to pay back a lot of its loans and has to succeed to do so. Banks are less willing to lend to these businesses, so they will have to find other types of finance.

Will banks lend and will shareholders invest?

Loans will be available to businesses but information about the business is required:

- The firms's trading records.

- Forecasts about the future.

- Forecasts have to show that the firms are solvent, i.e. able to repay the loan and the interest back.

Banks will also consider:

- Experience of the people running a business.

- Gearing ratio of a business.

This is what shareholders will consider if they want to invest:

- The future prospects of the company.

- How much dividends are given out compared to other companies.

- Trend of share prices.

- Gearing ratio.

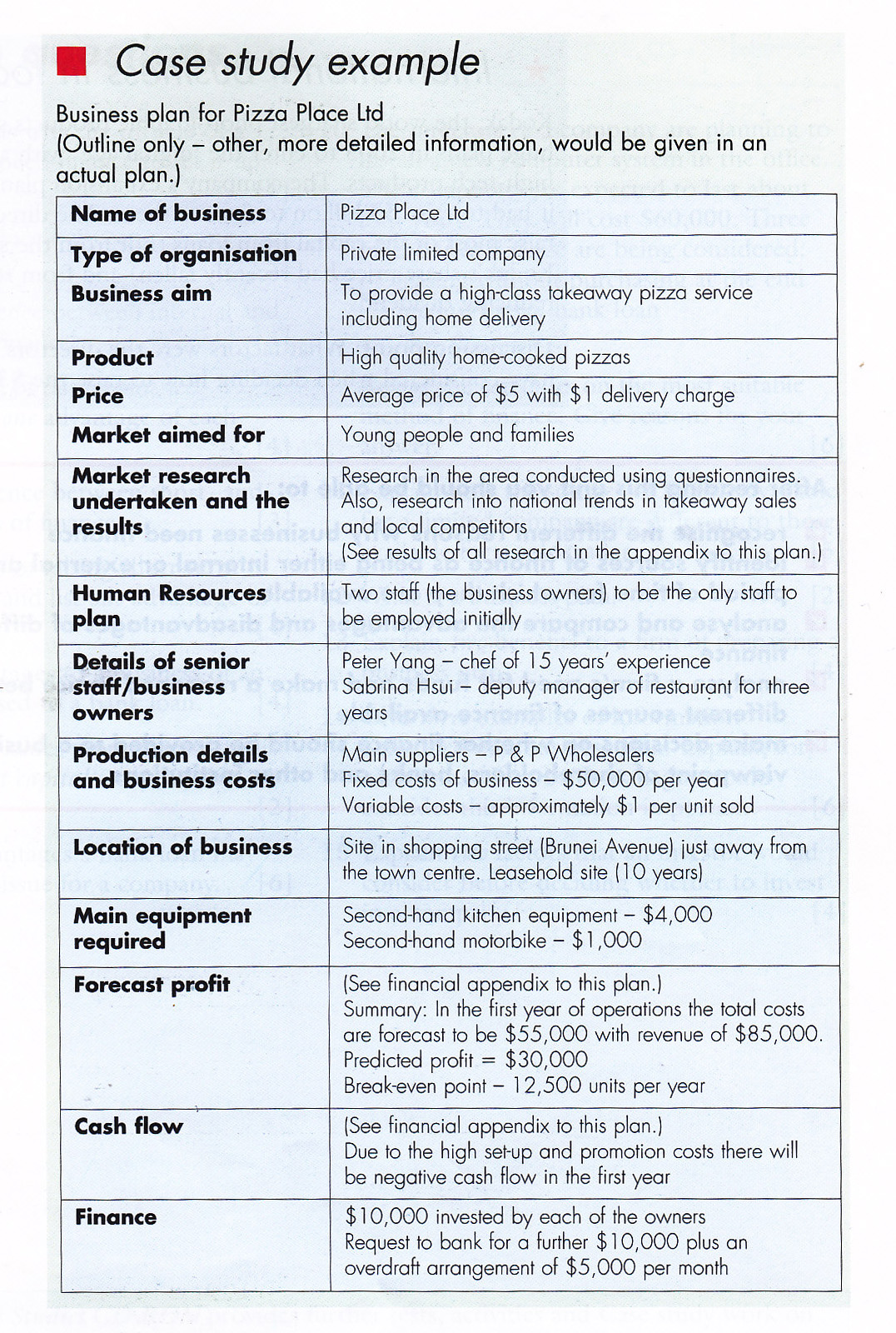

Business plans

Banks will want to see a business plan if they are to lend to most businesses, especially a newly created one. A business plan contains:

- Objectives.

- How the business will be operated.

- How the business will be financed.

By creating a business plan owners will have to think carefully ahead about their business to ensure the best plan possible. These are things they will need to consider:

- Target market and consumers.

- Profits, costs and break-even point.

- Location of the business.

- Machinery and workers required.

Without a detailed plan which works, bank managers will be reluctant to lend any money to businesses because their owners have not shown that they are serious enough about their business.

Here is an example of a business plan from the book, it shows the things you need to put in a business plan:

As a little reminder, this business plan is not mine, and all credit goes to the book and its author. Thank you

That's the end of chapter 9! If you want to view this page in 5 different dynamic view, click here.

================================================================

I luv u dude!!!! My savior.

ReplyDeleteGreat write-up, I am a big believer in commenting on blogs to inform the blog writers know that they’ve added something worthwhile to the world wide web!..project finance

DeleteThank you , I love you.....!!!

ReplyDeleteI love u too

DeleteThis type of analysis is really hard to create.Thankyou so much for your corporation and your help!

ReplyDeletethx dude!!! U did a great job...☻

ReplyDeletethank you sooooo very much!!

ReplyDeleteHave a mock exam tomorrow and thank heavens I found this! :D

I think this will help me a lot and hopefully I will pass! :)

Thank you so much :) Really did help me out!

ReplyDeleteTHANK YOU SO MUCH for spending time and creating this blog. Its extremely helpful!

ReplyDeletewhat is r&d ?

ReplyDeleteresearch and development :)

Deleteman....you are a fucking legend.

ReplyDeletehow did you find the time to do all this shit.

appreciate the effort though.

rather use your notes instead of the real book

YOU ARE FRICKIN AWESOME!

ReplyDeleteLogical analysis of a financial situation or plan from a tax perspective, to align financial goals with tax efficiency planning.

ReplyDeletebusiness tax planning

goooooooooooooooooooood fuckinggggggggggggg shit

ReplyDeleteGOD BLESS YOUR SOUL

ReplyDeletenext time there is no need of doing this

ReplyDeleteif you do again then get a big punch from me.

go to hell

don't think too smart

i can also copy from the book and publish here and can get good reviews from other people

we should spit on you

Maybe you should spit on yourself, rather than hating on a successful man publishing the best business study notes to the UK students and the worldwide, whom are benefiting. Why are u mad? if you really are jealous or something then go ahead, create your own damn amazing (not) notes. And leave successful people alone. You are nothing but shit in real life to be honest. Are you jealous because you got to know/review his notes late after you did your ig's or your parents haven't tought you how to be nice and thankful yet? If not then they should consider on doing that. And if not even, buy discipline and manners books that must be available in libraries all around. In conclusion, the publisher won't care to depress himself because of your lame comment so dont bother.

DeleteXO

GREAT JOB , I get high marks and I only study from this simple brief summary, THAN

ReplyDeleteU

This will help me in the finals....

ReplyDeleteStill Complicated as text book, while other chapters are well understandable!!!!!!

ReplyDeleteHow about trying to grow some brain cells first?

DeleteThank you, appreciate your effort.

ReplyDeleteyou could include the formula of gearing which is -

ReplyDelete(Long term liabilities ÷ Capital Employed) x100

2 entire years later, your wonderful notes are still helping students all across the world like me! A friend of mine showed me this website and it has been SO much help in making me understand the chapters. God bless you my friend <3

ReplyDeleteYou are an angel sent by god! Cheers loads!

ReplyDeletethank u sooooooo vry much u eally saved me dis is freeking awsum dude..i really appreciate u aloooot

ReplyDeleteOh thank God there is some one on earth who is helpful

ReplyDeleteI left my book at school and I was so tensed but after this I am 110% sure I will score the highest

the short-term, medium-term & long-term is legit? because my business teacher told me something else..

ReplyDeleteshort-term = maximum of 12 months

medium-term = more than 1 year but less than 5 years

long-term = more than 5 years

....... i'm confused????

basically he copied the book

ReplyDeleteThanks man. This was very helpful. I became a world topper in BS because of these notes. I owe the credit to you. Cheers!

ReplyDeletethanks bro this is freaking helping me in my homwork

ReplyDeletefor those that do not comprehend trade credit, what they mean by "an interest free loan" is ...

ReplyDeleteThe payment is delayed till further notice which would leave the business in a better cash position, the business receives goods from suppliers and delays payment , don't forget that the goods are items of value therefore in reality they are lending money to the business .

bro in my book it says internal an external comunication?????????////whts going on

ReplyDeletemagnificent issues altogether, you just received a new reader.

ReplyDeleteWhat would you suggest about your publish that you made a few days in the past?

Any positive?

pretty cool i like the font

ReplyDeletedamncool as shit

ReplyDelete